…consumption drops 17% as retail prices remain stable: Jan ₦950–₦1,550/kg vs Feb ₦980–₦1,500/kg

Oredola Adeola

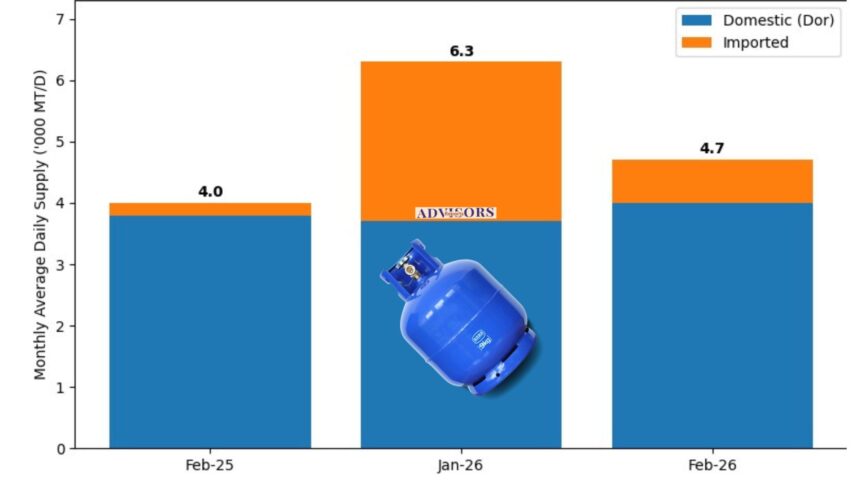

In February 2026, domestic producers—including the Dangote refinery, NLNG, and other local gas suppliers—accounted for approximately 85% of Nigeria’s total Liquefied Petroleum Gas (LPG) supply, contributing about 4,000 metric tonnes per day (MT/day), while imports made up the remaining 15% at 700 MT/day.

This revealed a strong and steady contribution from gas processing plants and the Dangote Petroleum Refinery and Petrochemicals complex (DPRP).

This was revealed by the Nigerian Midstream and Downstream Petroleum Regulatory Authority (NMDPRA) in its State of the Downstream Sector Fact Sheet for February 2026, compared with the data obtained by Advisors Reports in January.

Overall, the country’s average daily cooking gas supply for the month stood at 4,700 MT/day, compared to 6,300 MT/day recorded in January 2026.

The data showed a sharp decline in import dependency in February relative to January, with imports dropping from about 41% of total supply in January to 15% in February.

Domestic supply on the other hand increased its share from roughly 59% to 85%, even as total volumes moderated month-on-month.

Further analysis of the data shows that average daily cooking gas (LPG) truck-out declined to 4,194 MT/day in February 2026, compared to 4,860 MT/day recorded in January, indicating a moderation in downstream offtake.

Similarly, average daily consumption dropped to 4,194 MT/day in February from 5,050 MT/day in January, reflecting a broader slowdown in market activity.

Retail prices remained relatively stable across both months, with LPG selling between ₦950 and ₦1,550 per kilogram in January, compared to a slightly narrower range of ₦980 to ₦1,500 per kilogram in February.

On a year-on-year basis, domestic supply strengthened, with local producers delivering an average of 4,000 MT/day in February 2026, up from 3,800 MT/day in February 2025.

Imported volumes also increased year-on-year, rising to 700 MT/day from 200 MT/day over the same period.

However, month-on-month data highlights a sharp contraction in imports, which dropped significantly from an average of 2,600 MT/day in January 2026 to 700 MT/day in February, reinforcing the growing dominance of domestic supply.

Consistent with earlier trends, the February 2026 factsheet further confirms that throughout 2025 and into the first two months of 2026, Nigerian producers have remained the primary source of LPG supply.

In several peak periods—including February, March, and July—local production met nearly all national demand, with imports either minimal or entirely absent.